TLDR

From 1 July 2027, losses from residential investment properties can only offset other residential property income — not salary or wages. Properties held at the 12 May 2026 announcement keep current rules. Qualifying new builds keep full negative gearing access. The enabling bill was introduced to Parliament in May 2026 and is not yet law.

What Negative Gearing Is

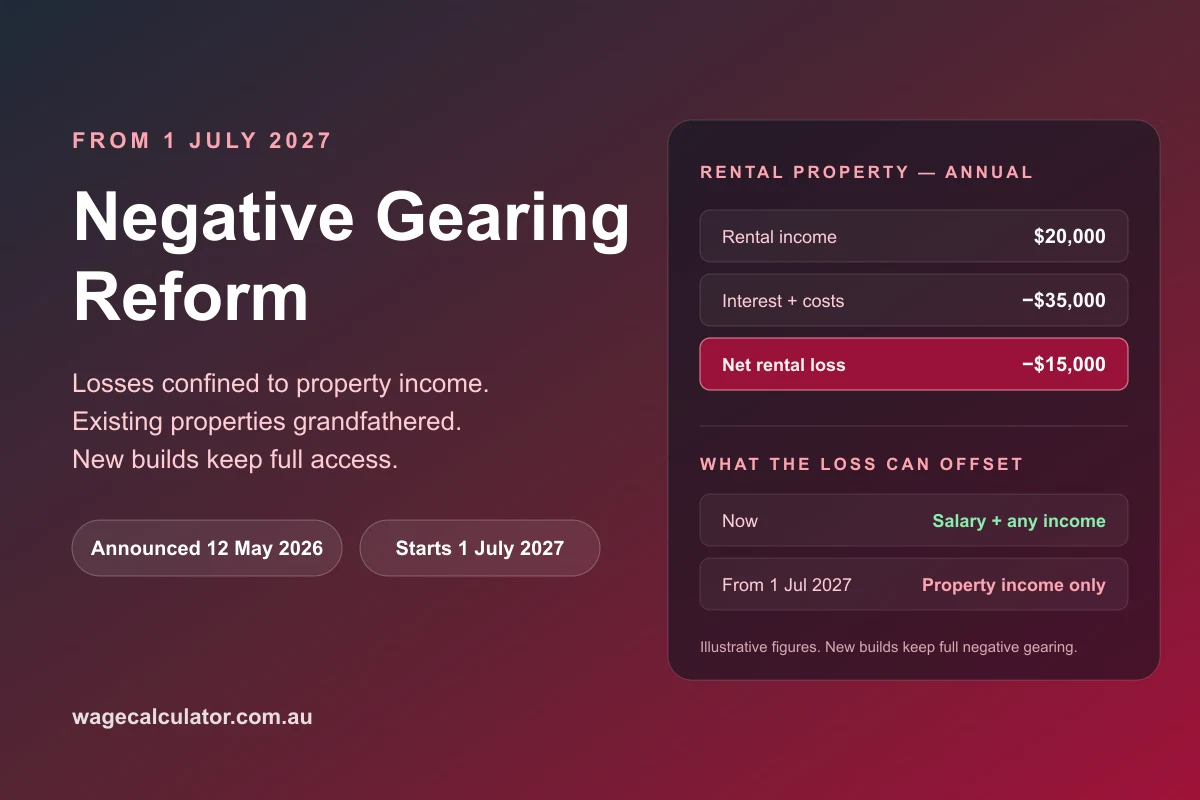

A property is negatively geared when its running costs — loan interest, management fees, maintenance, depreciation — exceed the rent it earns. Say a unit collects $20,000 in rent but costs $35,000 to hold: the investor makes a $15,000 loss. Under the current rules, that loss deducts from their salary, cutting their taxable income and so their tax bill. The investor wears the cash shortfall expecting capital growth to outweigh it at sale.

The 2027 reform doesn't abolish that mechanism — it narrows what the loss can offset. For affected properties the $15,000 loss could no longer reduce salary income; it could only offset other residential property income, including future residential capital gains, carrying forward until used.

Key takeaways for investors

- Losses confined to property income: From 1 July 2027, residential property losses can only offset other residential property income (including capital gains from residential property), not salary or other income.

- Three transitional bands: Properties held at 12 May 2026 keep current rules; properties bought between announcement and 30 June 2027 keep NG only during that window; properties bought from 1 July 2027 get no NG on established residential property.

- New-build exception preserved: Qualifying new builds retain full negative gearing access and the CGT election from the companion 2027 reform.

How the New Rules Work

The reform confines residential property losses to residential property income. Losses from an affected property can offset rent from any residential property you own, and capital gains from residential property — but not salary, wages, or business income. Excess losses carry forward without expiry until residential property income arises to absorb them.

Which rules apply to a given property depends entirely on when it was acquired — the three transitional bands below. The change interacts with the companion CGT reform at sale, covered in the 2027 CGT reform guide.

Transitional Bands

The reform creates three acquisition windows. Each determines whether negative gearing losses can offset salary income, only property income, or not at all.

| Acquisition timing | NG treatment | At sale / disposal |

|---|---|---|

| Held at 7:30pm AEST 12 May 2026 (including signed-but-unsettled contracts) | Current NG rules apply — losses offset any income. | Capital gains follow the companion 2027 CGT reform. The property is grandfathered for NG only. |

| Purchased after 7:30pm AEST 12 May 2026, up to 30 June 2027 | Full NG allowed only during this window. From 1 July 2027, losses can only offset residential property income. | Excess residential property losses carry forward to future years. |

| Purchased on or after 1 July 2027 (established residential property) | No NG against salary or other income. Losses only offset residential property income, with carry-forward. | New-build exception preserved — qualifying new dwellings keep full NG access. |

Source: Budget 2026-27 factsheet — Negative Gearing and Capital Gains Tax Reform (budget.gov.au).

New-Build Exception

Qualifying new builds retain full negative gearing access. The definition mirrors the new-build test in the 2027 CGT reform guide.

Worked Examples

A Treasury cameo and an illustrative transitional-window example show how the bands play out.

Michael — grandfathered existing investor

Michael owns a residential investment property purchased before 12 May 2026. Under the reform, his property is grandfathered — current negative gearing rules continue to apply for as long as he holds it. Any rental losses on this property can still offset his salary and other income, exactly as they do today. If Michael sells the property later, the CGT treatment follows the separate 2027 CGT reform rules.

Source: Treasury cameo, Budget 2026-27 Negative Gearing and CGT Reform factsheet.

Yoonseo — buying in the transitional window

Yoonseo buys a residential investment property in March 2027 — after the 12 May 2026 announcement but before 1 July 2027. She can negative gear normally during the transitional window. From 1 July 2027, her rental losses can only offset residential property income, including future capital gains from residential property. Excess losses carry forward to future years and can offset residential property income whenever it arises.

Illustrative example applying the transitional band rules in the Budget 2026-27 Negative Gearing and CGT Reform factsheet.

What's Not Changing

Super funds (including SMSFs), widely-held trusts and most managed investment trusts, commercial property, shares, and other non-residential asset classes are excluded from these changes.

What Investors Can Do Now

The reform affects different investor profiles differently. Below: what to consider for each. Whichever bucket you're in, state holding costs keep accruing alongside the federal rules — estimate the biggest one with the land tax calculator, since rental losses (where deductible) include land tax.

Existing investors holding pre-12-May-2026 properties

Your property is grandfathered. Current negative gearing rules continue to apply for as long as you hold it. No action required unless you're considering selling — at sale, CGT follows the separate 2027 reform rules.

Investors buying after 7:30pm AEST 12 May 2026, up to 30 June 2027

You can negative gear normally during this window. From 1 July 2027, losses on this property only offset residential property income. Plan cashflow on the assumption losses won't reduce your salary tax bill after that date.

Prospective buyers from 1 July 2027 (established residential)

Established residential property bought from this date offers no NG against salary. Losses only offset other residential property income, with carry-forward. Re-run yield assumptions before committing.

New-build investors (qualifying new dwellings)

Qualifying new builds keep full NG access plus the CGT election from the companion 2027 reform. The “qualifying new build” test is the same as in the 2027 CGT reform guide — vacant-land construction, knock-down rebuild with more dwellings, or new dwellings not occupied for >12 months before first sale.

This guide is not financial advice. For material decisions, consult a registered tax adviser.

Sources

Frequently Asked Questions

Is negative gearing being scrapped?

Not entirely. From 1 July 2027, losses from residential investment properties can only offset other residential property income (including capital gains from residential property), not salary or wages. Properties held at the 12 May 2026 announcement keep current negative gearing rules. Qualifying new builds keep full access. The reform reshapes how property losses interact with other income — it doesn't abolish negative gearing.

Is the negative gearing change law yet?

No. The Treasury Laws Amendment (Tax Reform No. 1) Bill 2026 implementing the reform was introduced to Parliament in May 2026 but has not passed. The ATO lists the measure as announced but not yet law. The rules described here reflect the bill and the Budget factsheet, and details could still change before the 1 July 2027 start date.

When does negative gearing end?

1 July 2027 is the start date for the new rules. Properties bought between the 12 May 2026 announcement and 30 June 2027 can negative gear normally during that window. From 1 July 2027, those same properties — plus any established residential property bought from that date — can only offset losses against other residential property income, with excess losses carrying forward.

Can I still negative gear my existing property?

Yes. If you held the property at 7:30pm AEST on 12 May 2026 — including signed-but-unsettled contracts — current negative gearing rules continue to apply for as long as you own it. The grandfathering is property-specific, not investor-specific. A new property bought after the announcement falls under the new rules even if you already own grandfathered properties.

Does this apply to shares?

No. The reform is specific to residential investment property. Share investments, ETFs, managed funds, commercial property, and other non-residential asset classes are unaffected by the negative gearing changes. Capital gains on those assets are subject to the separate 2027 CGT reform, but the loss-offset rules for them don't change.

What is a new build for negative gearing?

A qualifying new build is a dwelling constructed on vacant land, a knock-down rebuild that delivers more dwellings than the original, or a new dwelling not occupied for more than 12 months before its first sale. The definition matches the companion 2027 CGT reform new-build test. Qualifying new builds keep full negative gearing access — losses can still offset salary and other income — for first investor purchasers.

What happens to my losses?

From 1 July 2027, residential property losses can only offset other residential property income, including capital gains from residential property. Excess losses that can't be absorbed in the current year carry forward to future years. There's no cap on the carry-forward period — losses persist until residential property income arises to absorb them.