What counts as a genuine redundancy

A redundancy is genuine for tax purposes when your employer decides the job itself no longer exists and dismisses you because of that decision, and you are under Age Pension age (currently 67) on the day of dismissal. The label matters because only a genuine redundancy payment gets the tax-free limit below.

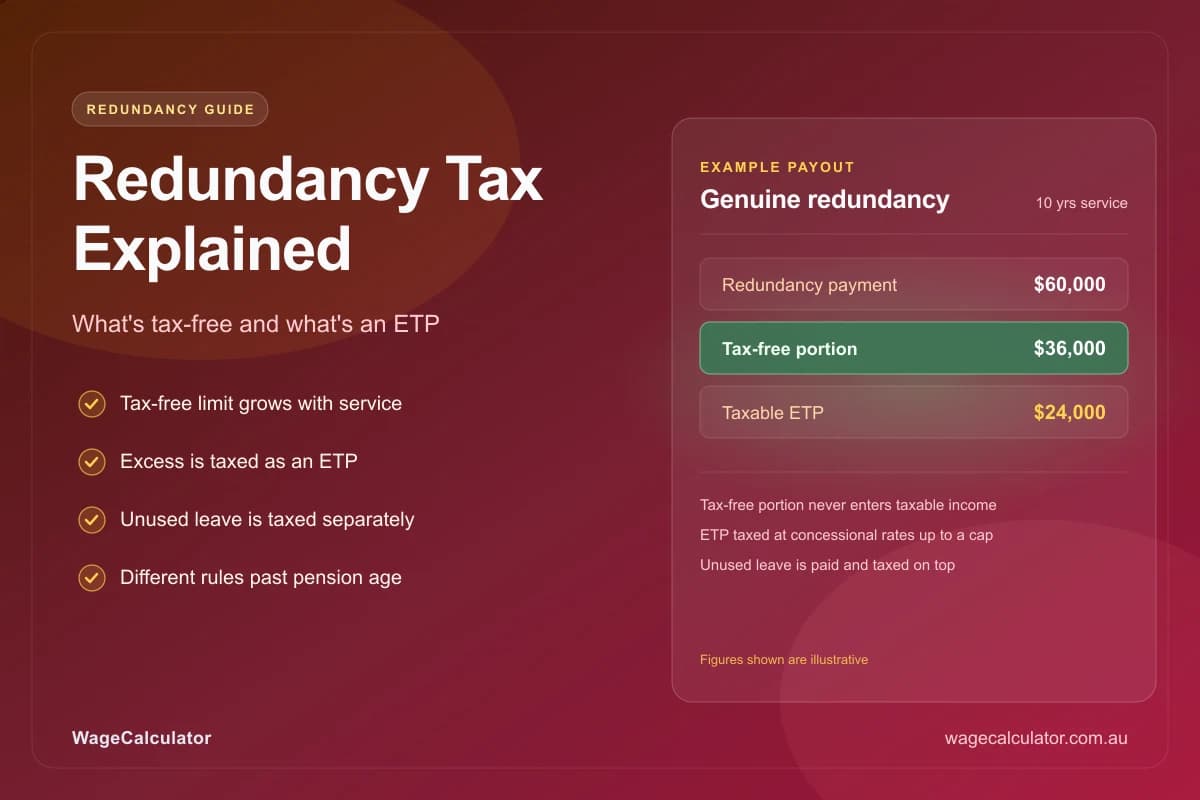

The payment itself can bundle several parts: severance based on weeks of pay per year of service, payment in lieu of notice, and a gratuity. Amounts owed to you anyway — ordinary wages, and unused leave — sit outside the genuine redundancy payment and are taxed separately. How many weeks you are owed in the first place comes from the National Employment Standards scale; the redundancy payout calculator applies it automatically.

Source: ATO — Genuine redundancy payments and Fair Work — Redundancy pay and entitlements.

The tax-free limit

Every genuine redundancy payment is tax-free up to a limit set by a simple formula: a base amount plus a service amount for each complete year you worked for that employer. For 2026–2027 the base amount is $13,598 and the service amount is $6,801 per year. Both are indexed to wages growth on 1 July each year.

Example: after 8 complete years of service, the 2026–2027 tax-free limit is $13,598 + ($6,801 × 8) = $68,006. A payout at or under that figure is entirely tax-free — it does not even appear in your assessable income.

Part years do not count toward the service amount, and the limit applies to the genuine redundancy payment as a whole — severance and any payment in lieu of notice combined, not each component separately.

How the excess is taxed (ETP)

Anything above the tax-free limit becomes an employment termination payment — a lump sum taxed at flat concessional rates instead of your marginal rate. The rate depends on your age, and the concession runs out at the ETP cap ($270,000 in 2026–2027).

| Portion of the taxable ETP | Your age | Withholding rate |

|---|---|---|

| Up to the ETP cap | Under preservation age (60) | 32% |

| Up to the ETP cap | Preservation age or over | 17% |

| Above the ETP cap | Any age | 47% |

The rates include the Medicare levy, and your employer withholds them before the money reaches you — there is no separate bill later unless other parts of your return change the picture.

Source: ATO — Schedule 11 tax table for ETPs.

Worked example: a $100,000 payout

Take a $100,000 genuine redundancy payment after 8 complete years of service, aged 45, in 2026–2027:

- Tax-free limit: $13,598 + ($6,801 × 8) = $68,006

- Taxable ETP: $100,000 − $68,006 = $31,994

- Tax withheld at 32% (under preservation age): $10,238

- In your bank: $89,762 — an effective rate of about 10.2% on the whole payout

The same payout at preservation age or older would be withheld at 17% on the excess instead. To run your own scenario, use the redundancy payout calculator.

Genuine vs non-genuine redundancy

A payment is non-genuine when you resign voluntarily, leave at the end of a contract, are dismissed for performance or disciplinary reasons, reach normal retirement age, or are Age Pension age (67) or older on dismissal. A voluntary redundancy still qualifies as genuine when the employer abolishes the role — volunteering for it does not disqualify you.

Non-genuine payments lose the tax-free limit: the whole amount is an ETP. They also face a second ceiling, the whole-of-income cap of $180,000, which is reduced by every dollar of other taxable income you earn in the same year — so a mid-year termination with months of salary already paid can push a large slice of the payment to the 47% rate.

Source: ATO — Genuine redundancy payments.

Leave, super and HECS

Three side rules catch people out. First, unused annual leave and long service leave paid out on a genuine redundancy are withheld at a flat 32% — outside both the tax-free limit and the ETP caps. Second, no superannuation is payable on redundancy pay, ETPs, or leave payouts, because none of them are ordinary time earnings — with one exception: payment in lieu of notice substitutes for ordinary hours you would have worked, so it does attract super.

Third, while the tax-free portion never enters your tax return, the taxable ETP and leave payments are assessable income — they can push your repayment income over a HECS/HELP threshold and trigger a compulsory repayment at assessment. The HECS/HELP repayment guide explains how repayment income is built, and the tax refund guide covers how the year reconciles.

Source: ATO — Schedule 7 tax table for unused leave on termination.

Frequently asked questions

Is redundancy pay taxed in Australia?

Partly. A genuine redundancy payment is tax-free up to a limit based on your years of service — for 2026–2027 the limit is $13,598 plus $6,801 for each complete year. Anything above that limit is an employment termination payment (ETP), taxed at a concessional flat rate rather than your marginal rate. Unused leave paid out at the same time is taxed separately.

How much of a redundancy payout is tax-free?

The tax-free limit is a base amount plus a service amount for each complete year with that employer. In 2026–2027 that is $13,598 + ($6,801 × years of service). After ten complete years the tax-free limit reaches $81,608, which covers many redundancy payouts entirely. Both amounts are indexed on 1 July each year.

What is an employment termination payment (ETP)?

An ETP is a lump sum your employer pays because your employment ended — the part of a redundancy above the tax-free limit, a golden handshake, or payment for unused rostered days off. It is taxed at flat concessional rates: 32% below preservation age or 17% at or above it, up to the ETP cap of $270,000 in 2026–2027 (non-redundancy ETPs like golden handshakes also face the whole-of-income cap, if lower). The portion above the cap is taxed at 47%.

What tax rate applies above the tax-free limit?

The excess is an ETP. If you are under preservation age (currently 60), your employer withholds 32%; at or above preservation age the rate drops to 17%. Those rates apply up to the ETP cap ($270,000 in 2026–2027); any amount above the cap is withheld at 47%, the top marginal rate including the Medicare levy.

Is super paid on redundancy payments?

Generally no. Redundancy pay, ETPs, and unused leave paid out on termination are not ordinary time earnings, so the superannuation guarantee does not apply to them. Your employer must still pay super on your normal earnings up to your final day, including any notice period you work. If you are paid in lieu of notice, that payment in lieu does attract super because it substitutes for ordinary hours you would have worked.

Is voluntary redundancy taxed the same as forced redundancy?

Usually yes. A voluntary redundancy can still be a genuine redundancy for tax purposes when the employer decides the role itself is no longer required and you are under Age Pension age. What disqualifies a payment is leaving by ordinary resignation, reaching normal retirement age, or dismissal for performance reasons — those are non-genuine and lose the tax-free limit entirely.

How is unused annual leave taxed on redundancy?

Unused annual leave and long service leave paid out on a genuine redundancy are withheld at a flat 32% rather than your marginal rate. They sit outside the redundancy tax-free limit and outside the ETP rules — they are separate payments with their own withholding schedule. Leave loading is included in the same treatment.

What happens if I am made redundant after Age Pension age?

From age 67 a payment cannot qualify as a genuine redundancy, so there is no tax-free limit. The whole payment becomes an ETP. You still get the lower 17% concessional rate because you are over preservation age, but a second cap applies: the whole-of-income cap of $180,000, reduced by other taxable income you earned in the year. Amounts above the applicable cap are taxed at 47%.