Which deduction method suits you

If you work from home or use your own car for work, you can claim the extra costs as a tax deduction — and for each there are two methods. A deduction reduces your taxable income, so its value depends on your marginal rate; the way income tax works sets what a claim is actually worth. The job is to pick the method that produces the biggest claim you can fully back up with records.

| Method | What you claim | Key record |

|---|---|---|

| Home office — fixed rate | 70 cents for each hour you work from home | Every hour worked from home, all year |

| Home office — actual cost | The actual extra running costs you can prove | Receipts, hours, and a private-use split |

| Car — cents per kilometre | 91 cents per work km, up to 5,000 km | How you worked out the kilometres |

| Car — logbook | Your business-use share of every car cost | A representative 12-week logbook plus annual odometer readings |

Home office: the fixed-rate method

The revised fixed-rate method lets you claim 70 cents for every hour you work from home in 2026–2027. That single rate bundles the running costs that are hard to split out — electricity and gas, home and mobile phone, internet, stationery and computer consumables — so you cannot also claim those items separately. You do not need a dedicated office; working at the dining table still qualifies, as long as you are genuinely doing your job and incurring extra costs.

Worked example

Source: ATO — Fixed rate method.

Home office: the actual cost method

The actual cost method claims the real additional expenses you incur working from home, rather than a flat hourly rate. You work out the work-related portion of each cost — energy per appliance, the work share of your phone and internet — and keep records for all of it. It takes more effort, but it can beat the fixed rate when your real running costs are high.

Either way, the decline in value of office furniture and equipment — a desk, chair, monitor or laptop — is claimed separately. An item costing $300 or less may be immediately deductible only to its income-producing use where it is used mainly to earn non-business assessable income, is not part of a set costing more than that amount, and is not one of identical or substantially identical items whose combined cost is higher. Otherwise, claim its decline in value over its effective life.

Source: ATO — Actual cost method.

Records for working-from-home claims

Record-keeping tightened on 1 March 2023, and what counts depends on your method. Under the fixed-rate method you must keep a record of the total actual hours you work from home across the whole income year — a four-week representative diary is no longer accepted. The actual cost method is more flexible: you can use either your actual hours for the year or a continuous four-week diary that represents your usual pattern. Either way, keep timesheets, rosters or diaries as you go.

For the fixed rate, you also keep at least one bill for each running cost the rate covers — for example one electricity bill and one phone bill — to show you actually incurred those expenses.

Source: ATO — Working from home expenses.

Car: the cents-per-kilometre method

For a car you own or lease, the cents-per-kilometre method pays 91 cents for each work-related kilometre, up to a cap of 5,000 kilometres per car each year. The rate is all-inclusive — it covers fuel, registration, insurance, servicing and the car's decline in value — so you cannot claim any of those costs on top. No receipts are needed, but you must be able to show how you reached your kilometre figure.

Worked example

One key limit applies to most methods: normal trips between home and your regular workplace are private commuting and usually cannot be claimed. Narrow exceptions can apply for genuinely itinerant work or essential bulky equipment where there is no secure workplace storage; simply choosing to carry equipment home is not enough.

Source: ATO — Cents per kilometre method.

Car: the logbook method

The logbook method has no kilometre cap. You keep a logbook for at least 12 continuous weeks that represents your usual travel pattern to work out your business-use percentage (work kilometres divided by total kilometres), then claim that share of your actual running costs — fuel, registration, insurance, repairs, interest and the car's decline in value. You can use it for up to five years only while the pattern remains representative and you keep opening and closing odometer readings for each year.

Worked example

Source: ATO — Logbook method.

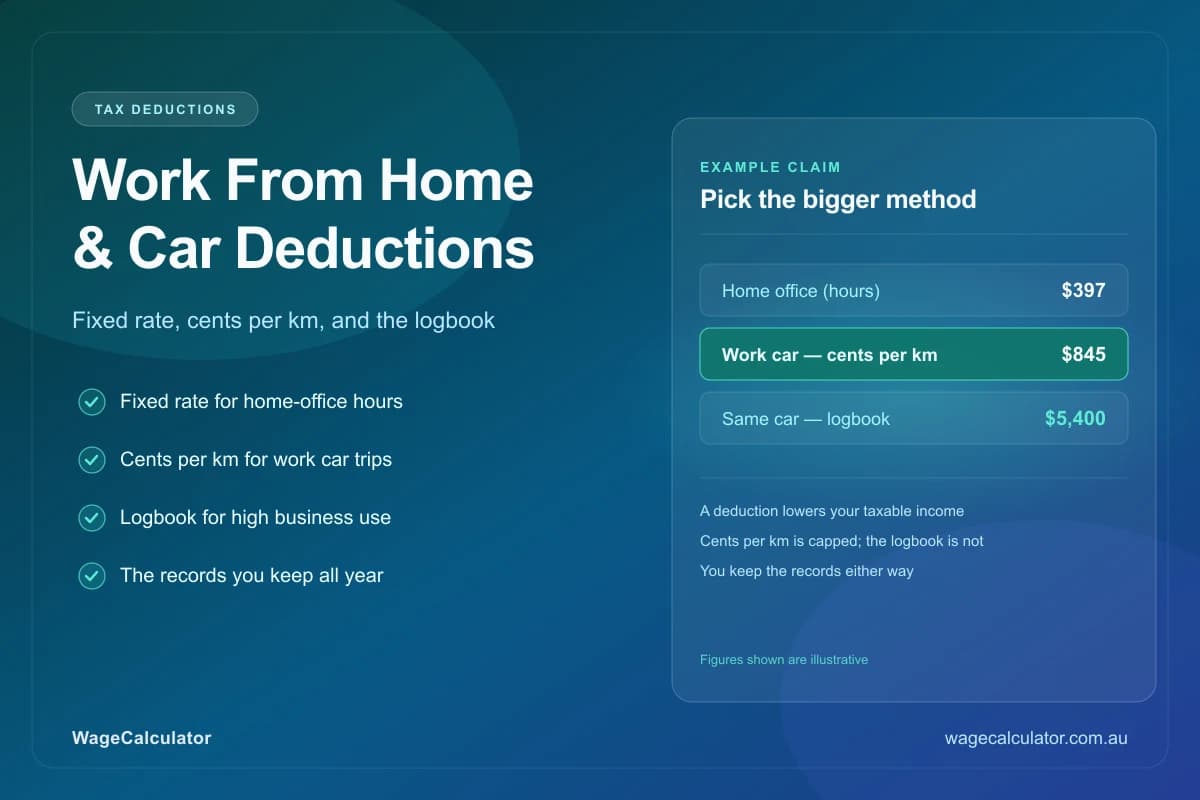

Cents per km vs logbook: which claims more

Cents per kilometre is simpler, but it is capped. The logbook is more work, but it scales with how much you actually drive for work and how expensive the car is to run. As a rule of thumb, once your genuine work travel pushes past the 5,000 km cap — or you run a thirsty or near-new car — the logbook tends to win.

| Cents per kilometre | Logbook | |

|---|---|---|

| Work travel | Up to 5,000 work-related km per car | Any distance — no cap |

| Records | A reasonable record of your work km; no receipts | Representative 12-week logbook, annual odometers and expense evidence |

| What you claim | 91 cents per km, covering all running costs | Your business-use % of actual costs, incl. depreciation |

| Best for | Occasional or low work travel | High work travel, or an expensive car to run |

Claiming both — and what you can't

Home-office and car deductions are separate, so a hybrid worker can claim both in the same return. They are also a common reason people see a bigger refund — the tax refund guide explains how deductions feed into the final result, and the tax return checklist lists what to gather first.

The commute trap

No double-dipping

For actual-expense claims, three rules apply: you must have spent the money yourself and not been reimbursed, the expense must directly relate to earning your income, and you must keep the required evidence for five years. The automatic standard work deduction is different: eligible people receive it without spending money or keeping deduction records.

Source: ATO — Records for work expenses.

Frequently asked questions

What is the work-from-home rate for the ATO?

For 2026–2027 the revised fixed rate is 70 cents for each hour you work from home. It bundles together your energy, home and mobile phone, internet, stationery and computer consumables, so you cannot also claim those running costs separately. The decline in value of office furniture and equipment is claimed on top. If your real costs are higher, the actual cost method lets you claim them with full records instead.

What is the cents per km rate this year?

The cents-per-kilometre rate is 91 cents for every work-related kilometre in 2026–2027, capped at 5,000 kilometres per car for the year. It is a single all-inclusive rate covering fuel, registration, insurance, servicing and the decline in value of the car, so you cannot claim those costs on top. You do not need receipts, but you must be able to show how you worked out your work kilometres.

Can I claim work expenses without receipts?

Not as an actual claim. The old exception that let you claim a small total of work expenses without written evidence was repealed from 2026–2027, and the automatic standard deduction replaced it: eligible residents get up to $1,000 of work-related deductions without receipts and without having spent the money. Claim actual work expenses instead and you need written evidence for the whole claim, not just the part above the standard amount — and it is only worth doing once your real costs exceed it, because anything you claim is subtracted from the standard amount rather than added to it. The rate methods are not receipt-free either: the fixed rate needs a record of every hour worked from home for the year plus at least one bill for each running cost it covers, while cents per kilometre needs a record of how you reached your kilometre figure but no receipts for the car costs.

Can you claim 5,000 km without receipts?

The cents-per-kilometre method needs no fuel or servicing receipts, and it is capped at 5,000 work-related kilometres per car each year. You still cannot simply claim the full cap — you must be able to show how you reached your figure, for example a diary of regular work trips. If your genuine work travel is higher than 5,000 km, switch to the logbook method to claim more.

Can I claim working from home and car expenses in the same return?

Yes. Home-office costs and work car expenses are separate deductions, so a hybrid or remote worker can claim both in the same year as long as each is genuinely work-related and properly recorded. Normal travel between home and a regular workplace is usually private and not deductible. Narrow exceptions can apply, for example for itinerant work or where essential bulky equipment must be transported because secure storage is unavailable; assess those facts before claiming.

Can I use both the cents per km and logbook methods?

For a single car in a single year you choose one method — whichever gives the larger, properly substantiated deduction. You can use different methods for different cars, and you can switch from year to year. Many people start with cents per km, then move to a logbook once their work travel climbs past the kilometre cap and the logbook clearly produces a bigger claim.

How do you work out a cents per km claim?

Multiply your work-related kilometres — up to the 5,000 km cap — by 91 cents. For example, a 20km round trip once a week for 48 weeks is 960 work-related kilometres, which at 91 cents a kilometre is $873.60. Keep a diary or record of the trips that make up the total so you can show the ATO how you reached the figure.

What can I claim if I work from home without a dedicated office?

You do not need a separate room or dedicated office to use the fixed rate method — working at the kitchen table still counts. You claim 70 cents for each hour you actually work from home, which covers electricity, gas, phone, internet, stationery and consumables. You can still separately claim the decline in value of a desk, chair or computer you bought to do that work.

Does the cents per km rate apply to electric vehicles?

Yes. Electric vehicles use the same 91 cents per kilometre rate, capped at 5,000 work-related kilometres, exactly like a petrol car. If you drive more work kilometres than that, the logbook method lets you claim your business-use share of actual running costs, including the electricity used to charge the car for work trips.